Pioneer Natural Resources’ $4.5 billion Acquisition of Parsley Energy

- Dec 2, 2020

- 7 min read

Updated: Dec 4, 2020

By Alexandros Assiotis (King’s College London), Jimmy Wang (Western University), Blanka Mona (University of Edinburgh), Buzz Fann (University of California, Los Angeles), and Steven Skomra (Georgetown University)

Deal Overview

Acquirer: Pioneer Natural Resources Company (NYSE: PXD)

Target: Parsley Energy, Inc. (NYSE: PE)

Estimated Value: $4.5B

Announcement Date: 10/20/2020

Acquirer Advisor: Goldman Sachs & Morgan Stanley

Target Advisor: Credit Suisse, Wells Fargo Securities

Pioneer Natural Resources Company, a large oil and gas exploration and production company is buying out Parsley Energy in a deal worth $4.5 billion ($7.6B including Parsley debt assumed by Pioneer). The all-stock transaction will be conducted under a fixed exchange ratio of 0.1252 Pioneer common stock shares for each share of Parsley common stock owned. The transaction includes a 7.9% premium to Parsley shareholders based on the closing share prices as of October 19, 2020. In total Pioneer will issue roughly 52 million shares of common stock in the transaction.

The new company will be 76% owned by Pioneer shareholders with the remaining 24% being owned by Parsley. With the completion of the transaction, Pioneer’s Board of Directors will increase to thirteen, the new additions to the board include Matt Gallagher, Parsley’s President and CEO and A.R. Alameddine, Parsley’s lead director.

The result of the deal, expected to finalize in Q1 2020, will create a gigantic producer in the Permian Basin, the heart of America’s crude oil boom. The Permian Basin is the world’s most productive oil field in the whole world, surpassing Saudi Arabia’s Ghawar Field. In 2019 the Permian Basin produced a record output of 1.5 billion barrels of oil. There is still a lot of untouched oil buried in the basin. The USGS estimated that there is roughly 46.3 billion barrels of oil and 19.9 billion barrels of natural gas liquids left to be discovered. The new company will be a Permian giant that is positioned to effectively capitalize on the oil-rich land. It will allow Pioneer to expand into the Delaware basin portion of the Permian, the location where most of Parsley’s resources reside.

Acquirer Company: Pioneer Natural Resources Company

Based in Irving, Texas Pioneer Natural Resources discovers, develops, extracts oil, natural gas liquids and gas operating mainly in the Permian basin. They mainly operate in the midland basin section of the Permian. According to figures given in Pioneer’s 2019 10K, the company had proved reserves of oil and gas totaling 1.315 billion.

Formed in 1997 through the merger of Parker & Parsley Petroleum Company and MESA Inc., under the ownership of T. Boone Pickens

CEO: Scott D. Sheffield

Employees: 2,323

Key Shareholders: The Vanguard Group, Inc. (10.48%), SSgA Funds Management, Inc. (5.97%), BlackRock Fund Advisors (4.84%)

Market Cap: $15.752B

EV: $17.99B

LTM Revenue: $7.65B

EBITDA: $2.29B

EV/Rev: 2.35x

EV/EBITDA: 8.71x

Target Company: Parsley Energy

Parsley Energy based in Austin, Texas is an oil and natural gas company operating in the Permian Basin specifically within the Midland and Delaware Basin. Based on their 2019 10-K they have oil, natural gas and NGL proved reserves of 592 million barrels.

Founded in 2008, by Michael W. Hinson and Paul Treadwell

CEO: Matthew Gallagher

Employees: 496

Key Shareholders: The Vanguard Group, Inc. (7.41%), Invesco Advisers, Inc. (7.37%), Boston Partners Global Investors (6.64%), Quantum Energy Partners (17.3%)

Market Cap: $4.98B

EV: $8.06B

LTM Revenue: $1.75B

EBITDA: $1.26B

EV/Rev: 4.59x

EV/EBITDA: -2.11x

Projections and assumptions

Short-term Consequences

With the price of oil stuck at around $40 a barrel in recent months and no recovery in sight, the oil industry has turned to consolidation. Pioneer’s acquisition of Parsley in an all-stock transaction valued at approximately $4.5bn is thus not a surprise. This merger will create the Permian Basin’s largest independent pure play exploration and production company. The combined company will become the 4th largest oil company in the world by both enterprise value and 2020E production.

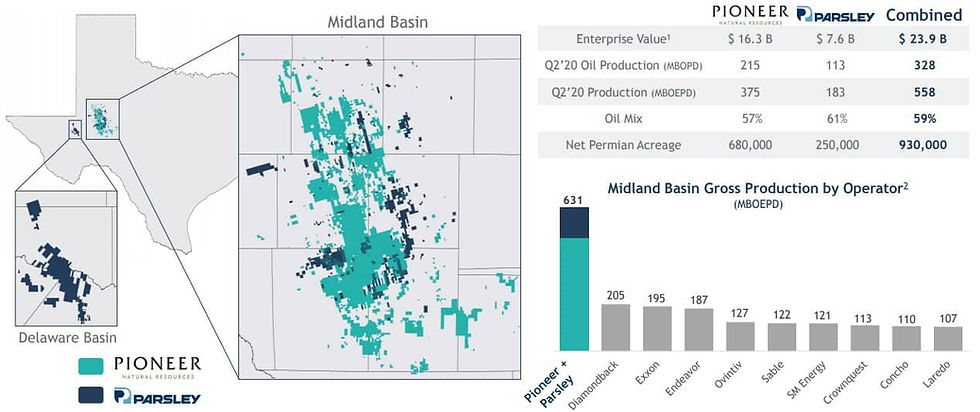

Figure 1: Combined Statistics

Pioneer expects annual synergies of approximately $325 million through primarily operational efficiencies and to a lesser extent from reductions in G&A and interest expenses. Over a ten-year period this amounts to expected present value cost savings of $2bn. One of the short-term immediate synergies associated with the transaction is the refinancing of Parsley’s existing debt at a lower interest rate, which is expected to lower interest expenses by around $75 million.

The transaction has been praised for its credit-friendliness and the positive impact it will have on Pioneer’s balance sheet. In particular, any added leverage from Parsley will be more than offset by its higher free cash flow. The strength of Pioneer’s pro-forma balance sheet will place it in a unique position relative to its peers in terms of its greater access to debt markets. This is particularly important as many oil companies currently lack the financial resources required to drill new wells and accommodate shifts in consumer demand.

Reactions to the transaction have been mixed. Shares of Parsley and Pioneer fell by 3.4% and 1.2%, respectively immediately after the announcement of the deal. Nevertheless, the companies’ share prices have recovered since then and even risen compared to the unaffected share price. Also, two of Parsley’s top shareholders have already voiced strong support for the deal. The 7.9% premium may have been a slight disappointment to some Parsley investors, but given the large degree of market uncertainty concerning the future of oil prices, the modest premium seems reasonable.

“At first blush, we think PXD is getting a solid deal as added leverage is more than offset by Parsley’s higher free cash flow given the low premium paid. The combined organization will be in a stronger position to garner capital relative to peers given the strength of the balance sheet and quality of long-term inventory.”

Analyst at Tudor, Pickering, Holt & Co.

Long-term Consequences

The Pioneer – Parsley combination continues a trend of consolidation that has been seen within the U.S. shale industry over the past few years, which has been even further accelerated as a result of the coronavirus pandemic. Historically low commodity prices for oil and gas have forced industry players to cut production volumes and improve efficiency levels while competing at below profitable prices, significantly impacting the cash flow generation capabilities and liquidity positions of many of the top players. Parsley specifically was forced to cut 20% of its annual production volume back in May, however, it was able to stabilize these volumes in June as a result of its low-cost position and hedging activities granting the company above market average prices.

As a result of the current industry state, mid-sized and larger competitors such as Pioneer have taken advantage of cheap acquisition opportunities in order to enhance economies of scale and better position themselves for price competition in the future, as smaller competitors work to prevent situations of financial distress and bankruptcy potential. Other completed deals in recent months include ConocoPhillips’ acquisition of Concho Resources, Chevron’s acquisition of Noble Energy, and Devon Energy’s acquisition of WPX Energy further highlighting the recent consolidation wave.

Additionally, low premium levels are the driving rationale behind further deal-making. Premiums on recent deals have ranged between 3% to 15% on average, far below industry premiums that have been seen in recent years. Pioneer’s acquisition of Parsley will represent a 7.9% premium, a significant discount that management teams see as a justification for acquisition spending in a currently struggling market environment.

Finally, the Pioneer – Parsley acquisition signals the important role that the Permian Basin will play in the future of the U.S. shale industry. The Permian is the largest and best-performing petroleum producing basin within the United States currently highlighting the need for industry competitors to increase their assets in the region. In November of 2020, the Permian region produced 4,336 thousands of barrels per day, representing 56.6% of total U.S. production. As it accounts for such a large percentage of production, recent deals have been concentrated within this region, however, this may soon begin to extend to other production basins as well. With Parsley being acquired by Pioneer, the new combined entity will become a Permian pure-play with over 930,000 net acres of land and over 558,000 barrels of oil equivalent per day (boepd) in total production capacity.

Figure 2: Barriers to Entry

Barriers to Closure

Initially, when this transaction was announced, there was some concern over a possible conflict of interest between these two companies. The President and CEO of Pioneer is Scott Sheffield, a veteran oil executive whose father-in-law was also a prominent wildcatter. Parsley’s founder and chairman, on the other hand, is Bryan Sheffield, the son of Scott. From the outside, this raises a number of concerns over the deal rationale and financing structure as a result of this uncommon family dynamic. However, Pioneer Chairman J. Kenneth Thompson noted in an interview that neither Scott nor Bryan was allowed to participate in the deal negotiations in order to lessen the possibility of a conflict of interest. Additionally, although the executives of Parsley will be entitled to a $13.8 million payout in stock as a result of this deal, Bryan will not be included due to his position on the board rather than as an acting executive. Even with these appeasements, this transaction will still be subject to an incremental layer of scrutiny from the board of each company before it is finalized.

There is also a general concern over corporate governance in the industry. Over the past few years, some oil companies have posted losses or gone bankrupt while their executives have made off with millions. Due to these occurrences, there is a possibility for more oversight from the SEC and other regulatory agencies in the future that could cramp the industry, even if this oversight does its job of cutting down on potential corruption.

In order for this deal to pass, it requires approval and acceptance from both boards of directors, as well as shareholders. Both are expected to approve the deal, which is projected to close in Q1 2021. It is noted that Quantum Energy Partners, Parsley’s biggest shareholder with a 17% stake, fully backs the deal.

Like many M&A deals this year, this transaction is threatened by the continued spread of the Covid-19 pandemic. With the pandemic growing its largest per day in many key countries like the US, and other countries beginning to shut down once again, there could potentially be issues in the market that cause this deal to collapse. An example would be an oil price collapse like the one that occurred earlier this year. Issues like this are not expected by any means, but in this period with so much uncertainty, it is always something to consider.

Comments